Local food has been the subject of federal, state, and local government policy in recent years as consumer interest in and demand for local foods has grown. In 2017, 130,056 U.S. farms (just over 6% of U.S. farms) were marketing food for human consumption locally through so-called direct-to-consumer (DTC) marketing channels, according to Census of Agriculture data. In Missouri, 3,640 farms (3.7%) had DTC sales. Online marketplaces could help farms who sell food directly to customers compete with other retailers by reducing the costs (such as time and transportation) of transactions at in-person markets such as farmers markets or other traditional markets. In-person marketplaces advantage farms located near urban centers because more rural farms have to travel longer distances to access customers.

Who uses online marketplaces?

The 2015 Local Food Marketing Practices Survey (LFMP) was the first of its kind to solicit data on the specific marketing channels used by “local” food farms. A second survey is planned to collect 2020 data. Using LFMP data, a MU Extension researcher and her colleague analyzed rates of online marketplace use as one type of DTC sales among farms. Findings include:

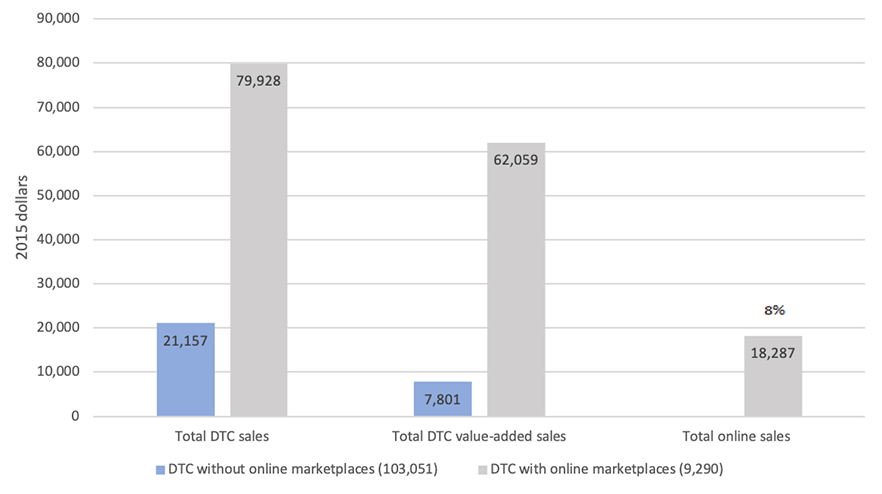

- 8% of DTC farms had an online marketplace, average online sales were $18,287 per year.

- Over 60% of DTC farms use the internet to access resources (i.e., purchase inputs, peer-learning, access business services, find funding opportunities, or obtain price/market information).

- Female farm operators were more likely to have an online marketplace, all else being equal.

- 35% of DTC farms were new to DTC. New farms (defined as those with fewer than 7 years of DTC sales) were more likely to have online marketplaces, perhaps because established farms have existing marketing channels and their business plan was not premised on online sales.

- New DTC farms with value-added product sales (e.g., bottled milk, wine, jam, cheese and meat) located in rural areas but adjacent to metro counties (metro-adjacent) were more likely to have an online marketplace than distant rural farms, all else equal. This suggests online and in-person marketing may be important for value-added farms.

- Among nonmetropolitan farms distant from metropolitan counties, those new to DTC marketing were 7% more likely to use an online marketplace than their more experienced counterparts.

- 85% of all DTC farmers were in metropolitan or metro- adjacent counties — thus, as of 2015, only 15% of local food farms were in the most rural areas of the country.

- Relative to nonmetropolitan farms with online sales, a greater proportion of sales from metropolitan farms with online sales were marketed locally — suggesting that accessing non-local customers is important for nonmetropolitan farms as their proximate customer base is smaller.

- Nonmetropolitan farms with online marketplaces were most likely to produce meat while metropolitan farms with online marketplaces were more likely to produce fruit and vegetables.

What do these findings mean for farms with food and value-added sales?

Even though rural farms have comparative advantages such as lower input costs, in-person DTC sales are more cost effective for farms near cities, according to prior research. Selling food online provides a chance for more rural farms to sell food directly to consumers without marketing and transportation costs that occur with in-person transactions, such as at farmers markets.

Findings suggests online marketplaces may be strategically important for rural farms that are new to DTC marketing and lack cost-effective access to urban DTC marketplaces. More experienced farms could have more brand awareness and loyal customers. Newer DTC farms could substitute the advantages of an established business for the advantages of a business model premised on online sales. Online sales offer farms the ability to reach a larger customer base as farms can engage with customers who may be near or far.

Understanding which farms use online marketplaces can increase the effectiveness of local food policy support.

What do these findings mean for consumers?

Purchasing food online may save consumers time. Online markets allow consumers to make purchases directly from farmers anywhere and at any time. For example, consumers who cannot attend a weekly farmers market can still buy food directly from their local farmers. Online purchases also allow consumers to buy hard-to-find products directly from farmers. Finally, the accessibility and availability of online products could result in increased competition and in-turn, lower prices and differentiated products which benefit consumer purchasing power.

What do these findings mean for rural broadband?

We were not able to assess the relationship between broadband expansion policies and online marketplace use by DTC farms due to data constraints. Even so, broadband policies have improved rural internet reliability, speed, and availability, which are preconditions for developing an online marketplace. Policies aimed at increasing broadband internet access reduce barriers to farms having online marketplaces.

For more information

The 2015 Local Food Marketing Practice Survey was conducted by USDA’s National Agricultural Statistics Service (NASS) in cooperation with other USDA agencies in 2016, using farmers’ data for the 2015 production year. The resulting data are the first nationally representative detailed data about specific marketing channels used by local food farms – farms that make direct sales of food to consumers, retailers, institutions, and/or intermediaries that market locally-branded food products. NASS used the phrase ‘local’ even though online sales are not geographically constrained. The sampling frame includes only local food farms, so we cannot make online marketing comparison with farms no selling locally; this study is limited to farms with direct sales of food for human consumption. Learn more about the data at https://agcensus.library.cornell.edu/census_parts/2012-2015-local-food-marketing-practices-survey/ (link updated 1/3/2022).

Source: O’Hara, Jeff and Low, Sarah A. (forthcoming). Online Sales: A Direct Marketing Opportunity for Rural Farms? Journal of Agricultural and Applied Economics.